If you’re a sole trader, chances are you’ve received an unexpected tax bill at some point. Calculating your own taxes can be complicated, and it’s easy to get it not quite right.

To help stop people from being hit with massive tax bills at the end of every tax year, the Inland Revenue Department (IRD) has set up a provisional tax system.

The tl;dr is that if you owe more than $5,000 in residual income tax for the previous financial year, you are required to pay your income tax in instalments (the ‘provisional’ bit of provisional tax) across the current financial year.

In theory, provisional tax helps you pay your income tax by spreading payments out. BUT while it does prevent a huge final tax bill, it can also be tricky to get right.

That’s why we’ve created this provisional tax explainer. We’ll cover what it is, what it’s used for, who needs to pay it, and how to get it sorted.

- What is provisional tax?

- Who needs to pay provisional tax?

- When are provisional tax payments due?

- How to get it right every time

What is provisional tax?

Provisional tax is the IRD’s tool to prevent huge tax bills at the end of every financial year. If you have a residual income tax bill of over $5,000, you’re required to pay provisional tax across the next financial year.

It’s important to note that provisional tax is not a separate tax. It’s the same income tax everyone knows and loves, just paid in instalments. The amount of each instalment is generally calculated based on previous year’s earnings or your estimation of your earnings in the current financial year.

If you earn irregularly, or you made an unusual amount of money in the previous financial year (good for you!), this could prove a problem – you may be required to pay more now than you’ll owe. But don’t worry, we’ll get to this in a moment.

Who needs to pay provisional tax?

If you owe $5,000+ in residual income tax (eg. tax not paid automatically throughout the financial year, like PAYE or withholding tax) after filing your tax return, then you’ll have to pay provisional tax in the next financial year.

Being subject to provisional tax means that you will need to make payments on a set schedule to ensure you’re paying your taxes in advance

Be careful here though – if you underpay your provisional tax it may result in fines and penalties.

When are Provisional Tax payments due?

Your provisional tax due dates will depend on two things:

- which payment option you choose (see below) and

- if you’re GST registered

The four payment options you can choose from are:

- The standard option;

- The estimation option;

- The ratio option; and

- The accounting income method (AIM)

The standard option

The standard option is the default option if you choose not to use the other options. It’s also often the better option for those who know their income will increase over the next year.

IRD will automatically calculate this for you, but in general, using the standard option, you:

- Start with your residual income tax amount

- Add a 5% uplift. If you haven’t filed your previous year’s returns, then it’s a 10% uplift

- Divide the resulting amount by the number of set instalments.

- You’ll usually have three instalments, but if you’re registered for GST and file semi-annual returns, then you’ll only pay two instalments.

- You’ll usually have three instalments, but if you’re registered for GST and file semi-annual returns, then you’ll only pay two instalments.

The estimation option

If you think your income will decrease over the next year, the estimation option could be right for you.

To use the estimation option, add up all the taxable income you think you’ll receive in the next year (including PAYE and self-employed income), minus any deductions you can claim, calculate the tax on that sum and subtract any PAYE and other tax credits you’re entitled to.

The number you’re left with will be your estimated residual income tax for the financial year – which is also the amount of provisional tax you have to pay. Divide this amount by the number of set instalments (like with the standard option, you’ll usually have three).

As per the IRD’s website, “if you do not think you’ll have any Residual Income Tax to pay, you can estimate your provisional tax at $0.”

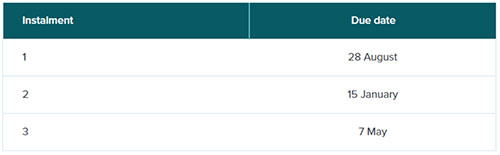

Payment dates for the standard and estimation options:

💡Remember, the IRD is pretty strict around these dates. If you fail to pay the right amount of provisional tax exactly when it’s due, you could face fines and/or penalties.

The ratio option

If your income fluctuates from high to low, then the ratio option could be right for you.

There are some fairly strict criteria around who can and can’t use the ratio option. To use the ratio option, you must:

- Have been registered for GST for the whole of the previous tax year, and part of the tax year before that (!)

- Have a RIT greater than $5,000 from the previous financial year.

- File your GST returns monthly or 2-monthly.

- Not have a partnership business structure

- Have a ratio percentage (calculated by IRD) between 0% - 100%.

Using the ratio option, you’ll pay provisional tax in 6 instalments according to the schedule below.

Payment dates under the ratio option

If you decide to use the ratio option you must let IRD know before the start of the tax year.

It’s also important to remember that IRD will calculate the ratio percentage for you by using the information they have from your GST returns and Residual Income Tax – so this option will only work when your tax and GST returns are up to date!

The accounting income method (AIM)

A less popular option is the accounting income method (AIM). The idea behind AIM is to prevent businesses with irregular or unpredictable income from having to make large payments at the end of the tax year.

Using the accounting income method, you only pay provisional tax when your business earns a profit. AIM uses an AIM-capable accounting software to automatically calculate your provisional tax payments for you, so this method only works as long as your financial records are up-to-date.

The due dates for AIM provisional tax payments are usually aligned with your GST due dates. If you file monthly GST returns, you’ll pay these monthly. If you pay your GST every two or six months, then you’ll make 2-monthly instalment payments.

How to get it right every time

We’re probably biased, but we really believe that the best way to sort your taxes is by using Hnry.

Hnry pays your taxes throughout the year, so you’ll never have to think about tax (provisional or otherwise!) again.

If the amount you earn fluctuates from month to month, Hnry automatically adjusts your income tax rate as you go to ensure that you pay the exact right amount of all your taxes – whenever you get paid.

That means:

- No more under or over-paying your Income Tax.

- No more worrying about your other taxes like GST or ACC levies – Hnry takes care of all your taxes for you, and files all your returns on your behalf

- No more eye-watering provisional tax payments, and no more uncertainty about how much money to hold back for taxes

- No need to pay for a separate accountant and multiple software tools to handle your financial admin – Hnry is an all-in-one service.

Our team of accountants and tax experts, and our award-winning software, have got your back.

Join Hnry today!

Share on: